Gold Price 2014 – How will the price of gold develop in the coming years?

In this millennium, the price of gold has risen sharply. Until 2012, gold price is risen each year for more than 10 years. But in the first months of 2013 the gold price decreased. How will the price of gold develop in 2014 and in the following years? We try a look into the future.

The past development of the price of gold

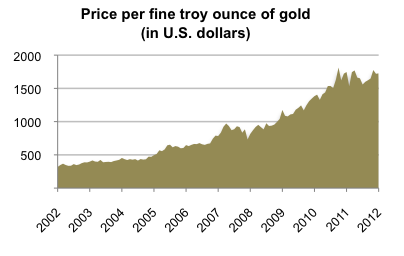

The gold price has risen in the past decade from 277 U.S. dollars (311 euros) at the beginning of 2002 to more than 1,000 US$ and up to a level of currently (April 3rd, 2013) 1,575 U.S. dollars per ounce. The price of gold has therefore grown by more than 450%. Thus, the price of gold has increased more than fivefold during that period.

In 2011, the price of gold has reached in September its highest level ever so far with a price of 1,895 U.S. dollars per ounce of gold. At the end of 2012, the price of gold was about 1,657 U.S. dollars (1,253 euros), more than 8% higher than at the beginning of 2012. Already in 2011, the gold price had risen by roughly 9%.

But in the first months of 2013 the gold price decreased – up to 3rd April by about 5% in US-Dollars and 2% in Euros. Is this the end of the long bull market?

The price of gold is determined by supply and demand

As it is the case with any other freely tradable good, the price of gold is determined by the demand for gold and the supply of gold. Basically, the gold demand and the supply of gold will always be balanced. In case of excess demand, the price of gold rises until demand matches supply. Conversely, in case of a surplus of gold, the price of gold goes down until the entire supply is in demand.

Demand for gold – the four pillars

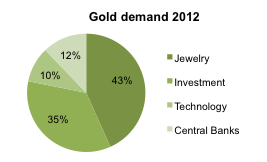

The demand for gold comes from four areas: the jewelry industry, demand for investment purposes, the industrial demand and demand from central banks.

In 2012, approx. 43% of the gold on the market was demanded by the jewelry industry. The second largest demand factor was the investment demand of the private sector with a 35% share of the total demand. It should be noted that particularly in the Middle East or Asian countries gold jewelry is often used in fact as a form of gold investment – and not only or primarily as jewelry in the original sense. In these parts of the world, the price of gold jewelry with typically high purity levels is often close to the value of the gold which is contained in the jewelry. Such gold jewelry is easily tradable and traded at a fair price and therefore suitable as a substitute for investment gold.

However, the share of the industrial demand for gold, for example from the wire technology or from dentistry, and the share of central banks in the total gold demand are only about 10% and 12% respectively.

Source: World Gold Council

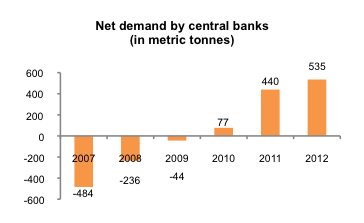

Looking at the development of the individual demand factors over the six years from 2007 to 2012, the industrial demand for gold for technological applications went from 462 metric tonnes in 2007 to 428 tonnes in 2012 (the low was 368 tonnes in 2009, the high was 466 tonnes in 2010). However, according to the World Gold Council, the demand for gold jewelry – traditionally the most important item of the total demand for gold – has declined by more than 20% during that time frame.

This decline in demand from the jewelry sector, however, was more than offset by an increase in demand from retail and institutional investors and the central banks: The investment demand increased – based on the demand for gold in metric tonnes – by almost 124% from 2007 to 2012, although -after it had risen from 2007 to 2011 – it fell in 2012 by nearly 10% compared to 2011. Central banks, which for years on balance sold more gold than they bought, reduced their gold sales and are since 2010 even net buyers of gold. In 2011, the purchases by the central banks were slightly higher than the total gold demand from the technology sector, in 2012 demand from central banks was significantly higher (535 metric tonnes versus 428 metric tonnes).

Source: World Gold Council

It is very difficult to forecast the demand for gold for 2014 and the coming years. The demand for gold jewelry comes in particular from Asian countries, especially India and China. In case of a positive economic development of these countries and increasing prosperity, the increase in jewelery demand should continue.

Investment demand, however, is rather developing in the opposite direction: In Western countries, gold is often seen as a store of value or as an insurance protection against crises. In times of economic uncertainty or even acute crises, demand for gold as an investment tends to increase. In recent years, gold – including products that provide outright ownership of physical gold – became more and more easily accessible for retail investors – through the advent of new financial products on gold, such as funds, as well as non-regulated products such as vaulted gold. These new products facilitate an increasing private demand for gold as an investment.

With regard to the demand for gold from central banks, there are several scenarios: On the one hand, the central banks of emerging market economies, in particular, could adjust their gold holdings further to the level of many developed countries. On the other hand, countries with a precarious debt situation may be forced to sell gold holdings in order to reduce their debt.

Supply of gold – mining and recycling

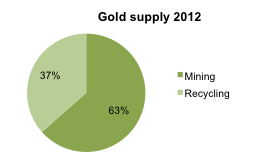

The supply of gold generally consists of the amount of gold mined annually and the amount of recycled scrap gold coming back into the gold market.

Source: World Gold Council

The current supply of gold is about one third higher than the supply of gold was 10 years ago. The actual mine production has increased only about 15%. However, the so-called “de-hedging” of mining companies was significantly reduced and resulted in an increased supply of gold available in the market (i.e, the mining companies themselves bought less gold to close open hedging positions). Compared to 2002, in 2012 the annual quantity of gold coming back into the market by way of recycling has almost doubled, because the rising price level made sales of scrap gold more attractive.

While mine production increased slightly in 2011 compared to 2010, the amount of recycled gold decreased in 2011, despite the high price of gold. One likely reason was that a large share of scrap gold holdings had already been sold over the last years. In addition, the “de-hedging” by the mining companies had finished. In 2012, supply from recycled gold and mine supply decreased slightly compared to 2011.

The mining of gold is getting less productive and more expensive due to less rich deposits, and for the next few years no significant increase of mining supply is expected. Thus, the supply of gold will remain rather constant in 2013 and 2014 and from a supply side perspective no negative pressure on the gold price is to be expected.

Momentum and fluctuations in the gold market

The total amount of gold ever mined worldwide currently has a value of about 9,000 billion U.S. dollars. Daily, only a very small part of this quantity is traded in markets. Therefore, sales or purchases of large quantities of gold hitting the market can affect the price greatly.

The emergence of new investment products and the activities of financial investors have made the gold price more susceptible to price fluctuations. The volatility of the gold price has increased significantly and there is no change in sight for 2014 and the next few years.

Trends and possible scenarios for the gold price

Due to the many supply and demand factors and their interdependencies, a reliable forecast of the future price of gold in 2013, 2014 and beyond is very difficult. Below, we discuss possible scenarios and trends as well as their potential impacts on the gold price.

Uncertainty and financial crises

The financial crisis has led to a sharp increase in demand from private investors and central banks. If the uncertainty persists or perhaps even escalates again, this could drive the gold price further up, for example in case of a possible euro-exit of Greece or an escalation of debt problems in other countries like the United States or Japan.

Inflation and depreciation of money

One argument of Western investors in favor of the purchase of gold is the fear of high inflation and thus a loss in value of money. In the wake of the debt crisis and the measures to ease monetary policy, this may be a legitimate concern, however, in recent years inflation has been low and some experts rather expect deflation than inflation in the short term.

In emerging economies, such as China or India, however, the situation is different: in those countries, the respective inflation rates are high by our standards – sometimes even in the high single or low double digits. This is not due to the debt crisis but due to the high economic growth in these countries.

Unlike in the developed economies, in China and India a strong investment (and jewelry) demand for gold is expected in case of a further positive economic development.

Normalization of the situation

Accordingly, in case of an economic recovery in the West – if there is a solution to the debt crisis – there would be opposing effects on the gold price: The very high investment demand would decline in the West and we could probably not expect to see a compensation by an increase in demand for gold jewelry.

In emerging countries such as China, a global economic recovery, however, should lead to further growth and thus greater demand for both gold jewelry and gold investments (which are used in these countries to hedge against local inflation).

War and political crises

A geopolitical crisis or a war – for example, a military strike by Israel against Iranian nuclear facilities – would probably quickly drive up the price of oil as well as the price of gold. Let’s hope that does not happen. After the election in the U.S., the likelihood of such an event has probably increased for 2013. Depending on the event and following developments, the effects on the price of gold may be very limited in time.

Demand from private investors

According to a study conducted by the scientists Claude B. Erb and Campbell R. Harvey, the value of all mined gold currently represents around 9% of the global wealth in stocks and bonds. However, if only investment gold is considered, the rate is just 2%. When looking at the investment behavior of individual investors, one notices that only a small number of investors is actually really invested in gold. If gold should continue to establish itself in the portfolios and assets held by private investors, this could lead to a large additional demand and consequently to a sharp rise in the gold price.

This trend could be facilitated by further new gold investment products which make an investment in (physical) gold easy for private investors. Such products include, for example, vaulted gold.

Behavior by the central banks

Predictions regarding the future demand from central banks are also difficult to make: in the wake of the debt crisis, countries such as Portugal could sell gold held by them, which could potentially result in a decrease of the gold price. On the other hand, a large part of the official sector demand in recent years came from central banks of (former) developing countries such as China. While Western countries such as Germany and the United States hold more than 70% of their reserves in gold, according to official data, this rate stands, for example in China, only at about 2%. The amount of gold held by China, however, has more than doubled – measured in metric tonnes – since 2000. If, for example, China would diversify its foreign exchange reserves further and invest a portion of them in gold, this could lead to a huge demand and could have a positive impact on the gold price.

In the so-called “Washington Agreement on Gold”, the central banks of many countries with large gold reserves and the Bank for International Settlement (BIS) and the IMF have agreed to sell only a specific quantity of gold annually. In 2009, the agreement was extended until the year 2014. Therefore, no negative price pressure is expected from this side in the short term but the mid-term outlook beyond 2014 is unclear.

Gold price predictions by analysts

The current analyst predictions regarding the price of gold for the years 2013 and 2014 differ, but seem to be mostly positive.

Hussein Allidina of Morgan Stanley’s, assumes early December 2012 that gold will be the most attractive commodity in 2013, and expects for 2013 an average price of 1,853 U.S. dollars per ounce. He justifies this with a weaker U.S. dollar due to the low interest rate policy and the purchase of mortgage-backed securities by the Federal Reserve on the one hand and the unlimited purchase of government bonds program of the ECB on the other hand, as well as with gold purchases by central banks, the high demand for gold ETFs and the recovery of gold demand in India.

Goldman Sachs, however, has recently reduced its forecasts for 2014 and now forecasts a gold price of 1,750 U.S. dollars per ounce. The bank considers it as likely that in 2013, the current gold bull market will end. It argues that the gradual rise in real interest rates due to the improved growth prospects for the U.S. economy is likely to more than compensate the impact of further monetary easing by the Fed.

At the beginning of October 2012, Deutsche Bank has raised its forecast for the price of gold for the years 2013 and 2014, justifying this with the unlimited purchase program of the U.S. central bank. Against this background, a rise in the gold price is only a matter of time. For 2013 the bank predicts a gold price of 2,113 U.S. dollars, for 2014 it forecasts a price of 2,000 U.S. dollars per ounce of gold.

Bank of America Merrill Lynch forecasts for the end of 2014 a gold price of 2,400 U.S. dollars. Key price drivers are expected to be interventions by the Fed and the European Central Bank. According to their analyst MacNeill Curry, the gold price could ultimately reach 3,000 to 5,000 U.S. dollars an ounce.

Following the decreasing gold prices in the first three months of 2013, many analysts and banks updated their forecasts and reduced their gold price targets. Societe Generale for example lowered its gold price forecast for 2013 from U.S. dollars 1,700.- to 1,500.- and reduced the price estimated for 2014 to U.S. dollars 1,400.- citing an economic recovery in the US followed by reduced stimulus measures as a key reason.

Conclusion for the gold price in 2014 and beyond

Like other asset classes, a gold investment is associated with risks. The price of gold can fluctuate strongly in the short term and also in the long term. Over very long periods of time gold does show a high and – from our perspective – unique stability or wealth preservation. However, such periods can be too long for individual investors.

On the other hand, for any risk averse investor an addition of gold contributes to the diversification of his/her investment portfolio. Due to the low correlation of gold with other asset classes, a gold investment reduces the (price) risk for the investor and therefore can reduce potential losses.

As is true with other forecasts, the future price of gold can not be predicted reliably. Analysts seem to be updating their forecast based on actual price developments rather than based on a real understanding of what the future will bring. The factors influencing the price of gold are varied and there are many interdependencies. In the event of a further escalation of the financial crisis or the emergence of new crises (e.g., North Korea, Iran), the price of gold may rise strongly as a result of the supposed function of gold as a “safe haven”. This might also be the case if the current economic uncertainties worsen again: generally speaking, uncertainty seems to be a good breeding ground for a rising gold price.

If, however, the current “bull market” stops, for example, following a solution to the global financial problems and a continued economic recovery, the gold price could also decrease potentially over many years or even decades, until one day very likely the next upturn will start.

Professional and courageous investors can speculate on a specific gold price development. For safety-oriented investors it is from our view recommendable – also in light of the lack of a regular income or interest from a gold investment – to see gold rather as a form of insurance. Unlike possibly individual stocks, bonds and other securities, gold will never lose its value completely. But conservative investors should invest only a portion of their total assets in gold.

As with all investments, investors have to consider cost and safety aspects when choosing a specific form of gold investments. The cost of buying and the annual costs of a gold investment can greatly affect the rate of return and thus have a big impact on the final value of the investment at the time of sale.

With regard to the safety of an investment, investors should not only take the possible price of gold into consideration but also potential risks that may be limited to certain products or suppliers. On our website, we compare prices and safety aspects of various vaulted gold products on the basis of transparent criteria.

[Last update: April 4, 2013]